Leveraged loan amend-and-extend volume surges to $106bn in H1

Leveraged loan borrowers are extending maturities at a record pace to avoid elevated refinancing costs, with an increasing share of stronger, private-equity-backed companies leading the charge.

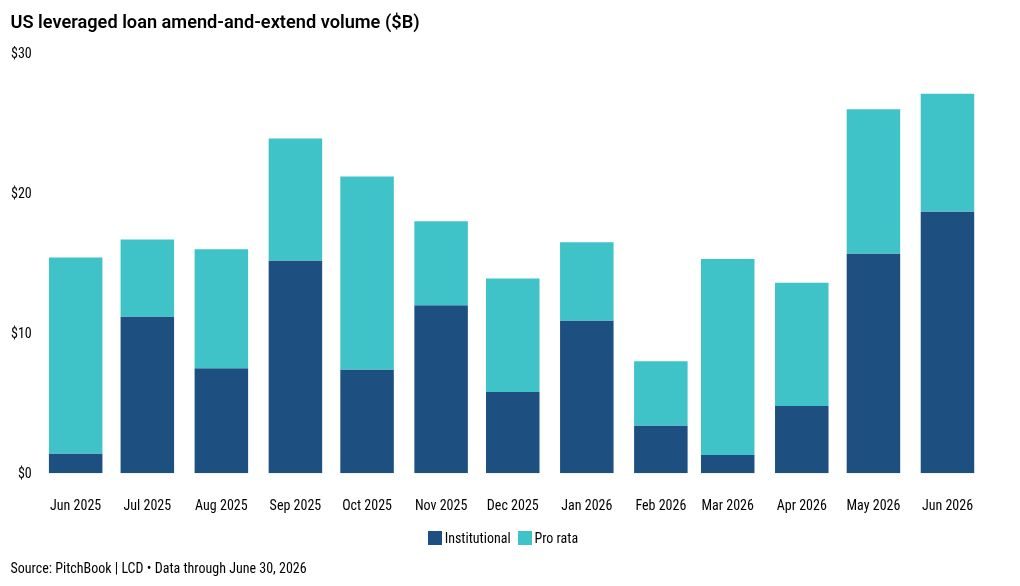

Leveraged loan issuers executed $27 billion of amend-and-extend transactions in June, bringing first-half volume to a record-setting $106 billion. According to LCD, this pace significantly exceeds the roughly $84 billion recorded over the same period last year. Last year was the second-busiest year on record for such activity, trailing only 2024. June's activity comprised 24 individual deals, edging up from 21 in May.

The primary driver behind this surge is a straightforward cost calculus for corporate treasurers. While the average yield to maturity for refinancing institutional term loans has fallen to 6.7% this year from a peak of 8.6% in 2024, rates remain well above the pre-2023 norms seen throughout 2011 to 2022. For many companies, paying a modest fee to extend existing debt is significantly cheaper than fully refinancing and marking the entire loan to current market spreads.

Market timing is playing an equally important role in issuer strategy. "Borrowers are also trying to be proactive and bring their deals to market before a new event that triggers risk-off sentiment, such as the AI-related selloff from a few months ago," said a market participant. By pushing back maturities now, companies are attempting to insulate themselves from potential future volatility in the credit markets.

This maturity push is not being led by distressed companies scrambling for survival, as the credit quality of borrowers utilizing this mechanism is actually improving. In 2026, 30% of amendments were executed by issuers rated BB-minus or higher, a sharp increase from just 11% last year. Simultaneously, the share of lower-quality B-minus borrowers dropped to 27% from 44% in the prior year, while B and B-plus credits grew to 39% from 33%.

Private equity sponsors continue to anchor this market. Sponsored borrowers drove $43 billion of the $55 billion in year-to-date institutional volume, maintaining a roughly 79% market share that is consistent with full-year 2025 levels. Institutional term loans, which are structured for buyers like collateralized loan obligations, saw $39 billion of volume in the second quarter alone. This represents the strongest quarterly showing in the recent data series.

For the first half of the year, institutional and pro rata volumes have reached a near-even split at $54 billion and $52 billion, respectively. Pro rata debt, which consists of amortizing term loans and revolving credit facilities typically held by banks, accounted for $8 billion of June's total. The balanced distribution underscores that the urgency to address near-term maturities is widespread across different segments of the leveraged finance market.