Africa private capital rebounds as middle market shrinks, exits stall

African private market deal volume jumped 19 percent in the second quarter, but a sharp drop in exits and a hollowing out of the middle market signal underlying stress for investors.

African private capital markets logged 221 transactions in the second quarter of 2026, a 19 percent increase from the first quarter. However, aggregate disclosed value dropped to $10.8 billion from $16 billion in the prior period, excluding massive first-quarter outliers like MTN’s $6.2 billion acquisition of IHS Holding assets.

For investors, the most pressing concern is a severe liquidity squeeze. Only seven exits were recorded in the quarter, the lowest since late 2022 and a sharp fall from 32 in the final quarter of 2025. This pullback dragged Stears’ proprietary liquidity gauge, the SVL Index, to 82.46, its lowest reading in years, though the firm cautions that reporting lags may eventually add to the total.

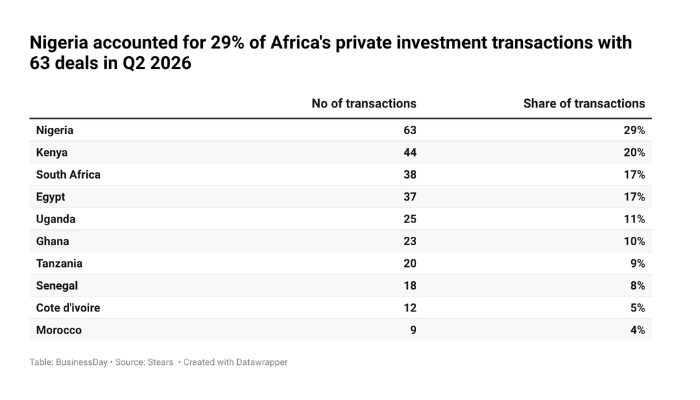

Nigeria cemented its position as the continent’s top destination, accounting for 63 transactions. The country captured $8 billion of West Africa’s $8.9 billion in disclosed deal value, driven by notable financings like a $600 million facility to Dangote Group’s Greenview Fertiliser Corp. Kenya, South Africa, and Egypt each held a 17 to 20 percent share, with Egypt showing the tightest domestic concentration.

Beneath the headline volume growth, the market's structure is shifting toward a barbell shape. Deals below $2.5 million became the largest ticket-size band, while mega-deals above $75 million held steady at 24 transactions. “The middle bands were comparatively squeezed even as activity improved elsewhere,” Stears noted, with the $2.5 million to $75 million bracket falling to 37 percent of disclosed deals from 54 percent in the first quarter.

Capital remained highly concentrated in familiar sectors. Financial services, industrials, energy, consumer discretionary, and information technology accounted for 82 percent of all activity. Payments infrastructure dominated sub-sector value at $3.0 billion, while telecom infrastructure and utility-scale solar also attracted significant capital.

Mergers and acquisitions cooled to 14 percent of total deals, headlined by the $2.7 billion acquisition of Payoneer and smaller artificial intelligence-focused takeovers. For fund managers, the combination of a shrinking middle market and stalled exits raises fundamental questions about return timelines, even as overall deployment activity superficially improves.