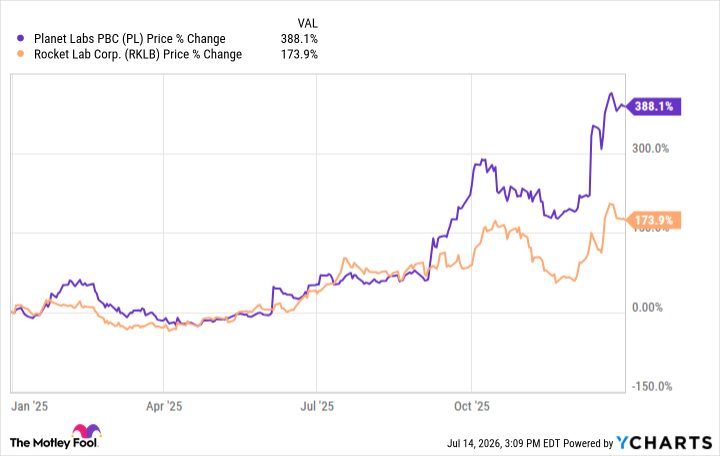

Rocket Lab Surges 388%, But Sky-High Valuation Risks Loom

Rocket Lab and Planet Labs posted massive 2025 gains fueled by the SpaceX IPO, but towering price-to-sales ratios and potential rate hikes pose significant risks for investors in 2026.

Rocket Lab and Planet Labs surged 388% and 174% respectively in 2025, driven by a record-breaking initial public offering from SpaceX. The blockbuster listing ignited a broader investing frenzy, drawing capital into adjacent space companies despite their lack of profitability.

However, both stocks have surrendered some of those gains over the past month. The recent pullback underscores a growing consensus that speculative excess, rather than current financial performance, is underpinning the sector.

A shift in macroeconomic conditions could accelerate this downturn. If the Federal Reserve raises interest rates this year, risk appetite across markets is likely to contract. Highly valued, unprofitable technology and industrial plays typically suffer the most in such environments.

Rocket Lab serves as a prime example of these stretched valuations. The company, which builds satellites and provides launch services to government and commercial clients, currently commands a market capitalization approaching $50 billion. That valuation rests on trailing 12-month revenue of just $660 million.

This dynamic translates to a price-to-sales ratio of approximately 75. For a company that has yet to record a profit, that multiple demands flawless execution over a multi-year horizon. It also assumes that revenue growth will rapidly scale to justify the premium investors are paying today.

To be sure, Rocket Lab possesses tangible fundamental catalysts. The firm holds a substantial $2.2 billion backlog and maintains strategic partnerships with NASA and various international space agencies. These contracts provide a visible revenue runway that separates it from purely conceptual space ventures.

Operational milestones also feature prominently in the bull case. Rocket Lab is preparing to launch its reusable Neutron rocket by the end of this year, although the timeline has already experienced several delays. A successful debut would significantly enhance its competitive positioning against larger launch providers.

Additionally, the company recently acquired Iridium Communications. This strategic move expands Rocket Lab's satellite network and launch infrastructure, transitioning it into a fully integrated, end-to-end space systems company.

Ultimately, the long-term narrative for space commerce remains compelling. Yet, at a 75x sales multiple, Rocket Lab's stock price already prices in a flawless transition from development-stage enterprise to cash-generating industrial powerhouse. Until the company demonstrates an ability to convert its robust backlog into actual earnings, the current valuation leaves investors heavily exposed to a market correction.