Cincinnati's $1.9bn rail fund barred from housing

A $1.9bn windfall from the sale of Cincinnati’s railway to Norfolk Southern is legally trapped by state lawmakers, leaving the city unable to fund new housing despite leading the US in rent inflation.

Cincinnati has secured a $1.9bn infrastructure trust from the sale of its municipal railway to Norfolk Southern, but state lawmakers have strictly barred the city from deploying any of that capital toward new housing.

The 2024 transaction resolved a protracted financial dispute. Norfolk Southern had previously offered $500m for the line in 2009, but by 2022, the city was demanding $65m annually for a lease renewal rather than the $25m the railroad was paying. Faced with a $400m deferred capital maintenance bill, the city opted to sell. The resulting trust generates $56m to $58m a year in investment revenue, effectively offsetting $388 in taxes for each of Cincinnati's 315,000 residents.

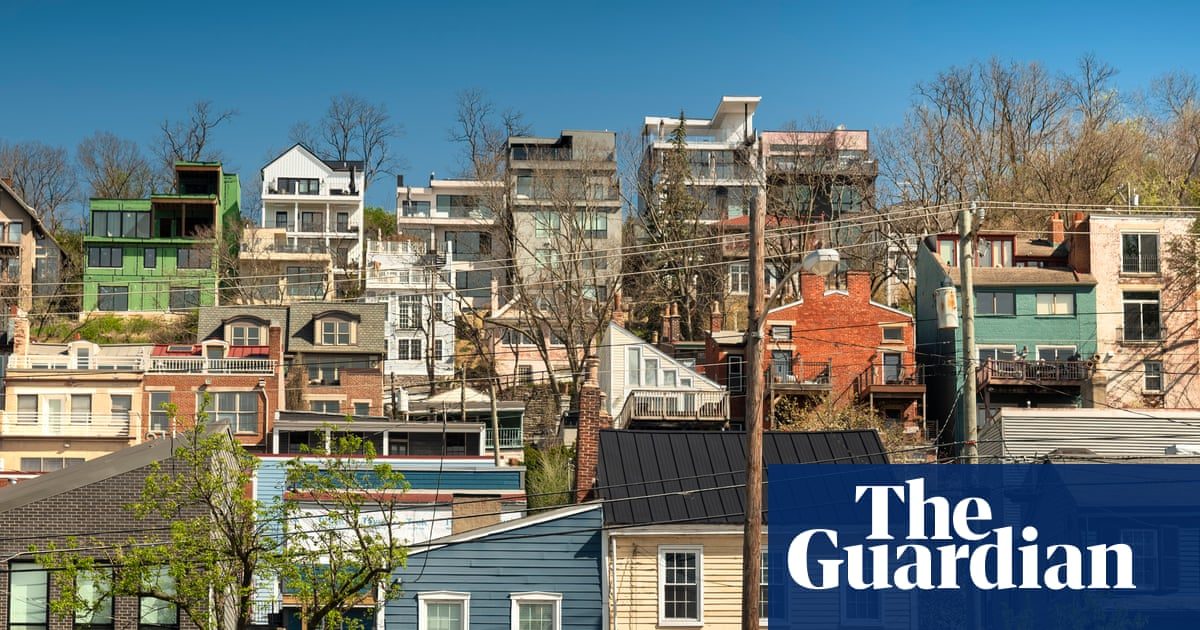

However, those tax offsets offer little relief to a residential market under severe strain. After decades of post-industrial population decline, Cincinnati is finally growing again. That demand shock has collided with a stagnant housing supply. Cincinnati recorded the highest percentage increase in average rental costs in the US in 2025. “You would expect that to be New York or Miami or San Francisco,” said Mayor Aftab Pureval. “Because we’re such an old city, we’re losing housing stock and not building housing fast enough, so we actually have less housing.”

State Republicans imposed the spending restrictions as a condition of authorizing the sale, limiting the fund to repairing existing assets like streets and parks. Former Republican state lawmaker Bill Seitz noted the safeguards prevent the money from becoming a “political slush fund,” citing a belief that the Democratic city council would “fritter it away on boondoggles.” State senator Louis Blessing acknowledged the broader partisan dynamic, noting Republicans view such cities as “very blue liberal havens” that need to be “saved from themselves.”

For real estate investors and municipal bondholders, the situation underscores a rising structural risk in American urban markets. When state legislatures interpose strict capital controls on municipal windfalls, cities are left unable to fund supply-side solutions to housing crises. Even with a $1.9bn endowment representing roughly $5,000 per resident, political friction can entirely prevent a city from addressing its most acute economic bottleneck.