Williams-Sonoma margins dwarf RH in weak home goods market

Williams-Sonoma is pulling ahead of RH in the home furnishings sector by converting sales into profit far more efficiently, a critical advantage as macroeconomic pressures suppress consumer demand.

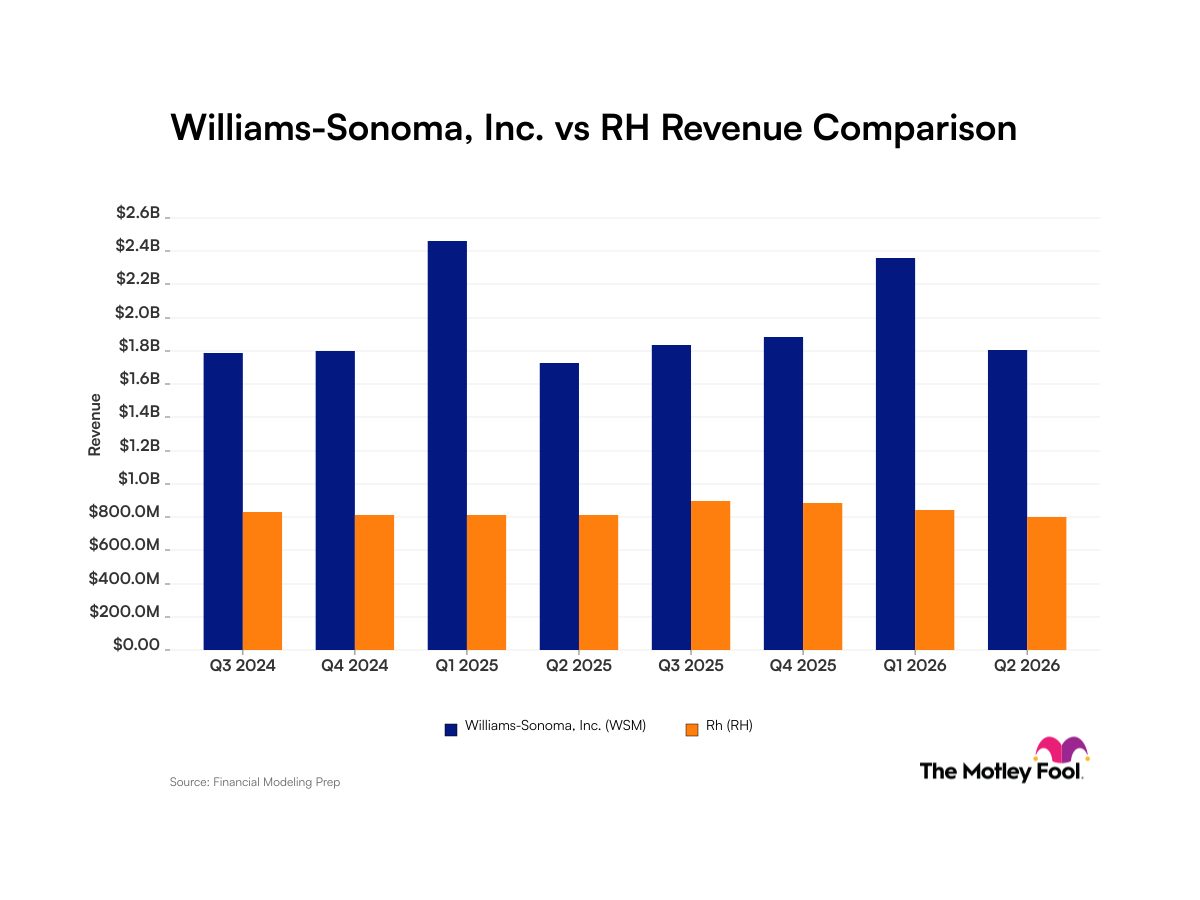

Williams-Sonoma reported a roughly 13% net income margin for the quarter ended May 3, 2026, starkly outperforming rival RH, which posted an EBIT margin of about 4% for the period ended May 2. This profitability gap has driven Williams-Sonoma's shares to significantly outperform RH's, which has seen its stock price tumble.

The diverging stock performance highlights how operational efficiency is separating winners from losers in the home goods sector. Inflation and elevated interest rates have consistently stifled consumer spending on furnishings over recent years. In this environment, top-line revenue growth has largely stalled across the industry. Because revenue serves as the most fundamental measure of a company's scale and demand, the inability of either retailer to expand the top line has shifted investor focus entirely toward margin preservation and bottom-line execution.

For Williams-Sonoma, the ability to convert flat revenue into a roughly 13% net income figure signals strong cost discipline and pricing power. The company achieved these margins while simultaneously managing a product recall and launching a new brand aimed at the dorm room market. Furthermore, its comparable store sales grew 4.8% year over year in the most recent quarter. This metric, which isolates the performance of existing locations, indicates that Williams-Sonoma is actively capturing market share from competitors despite the broader weakness in home goods demand.

RH is pursuing a different strategic path, prioritizing physical expansion with new international gallery openings in Milan and London alongside its catalog and online platforms. However, this capital deployment has not yet yielded the same financial returns. Generating only an approximately 4% EBIT margin suggests RH is absorbing heavy operating costs that are dragging down overall profitability. Until this international footprint scales sufficiently, the company remains vulnerable to the same macroeconomic headwinds that are suppressing demand.

For market professionals evaluating these stocks beyond 2026, the contrast underscores a shift in sector valuation metrics. Future catalysts for Williams-Sonoma rest on sustaining its comparable sales momentum and defending its newly acquired market share. RH faces the taller task of proving that its international gallery investments can eventually translate into the kind of margin expansion that currently eludes it.